All Categories

Featured

Table of Contents

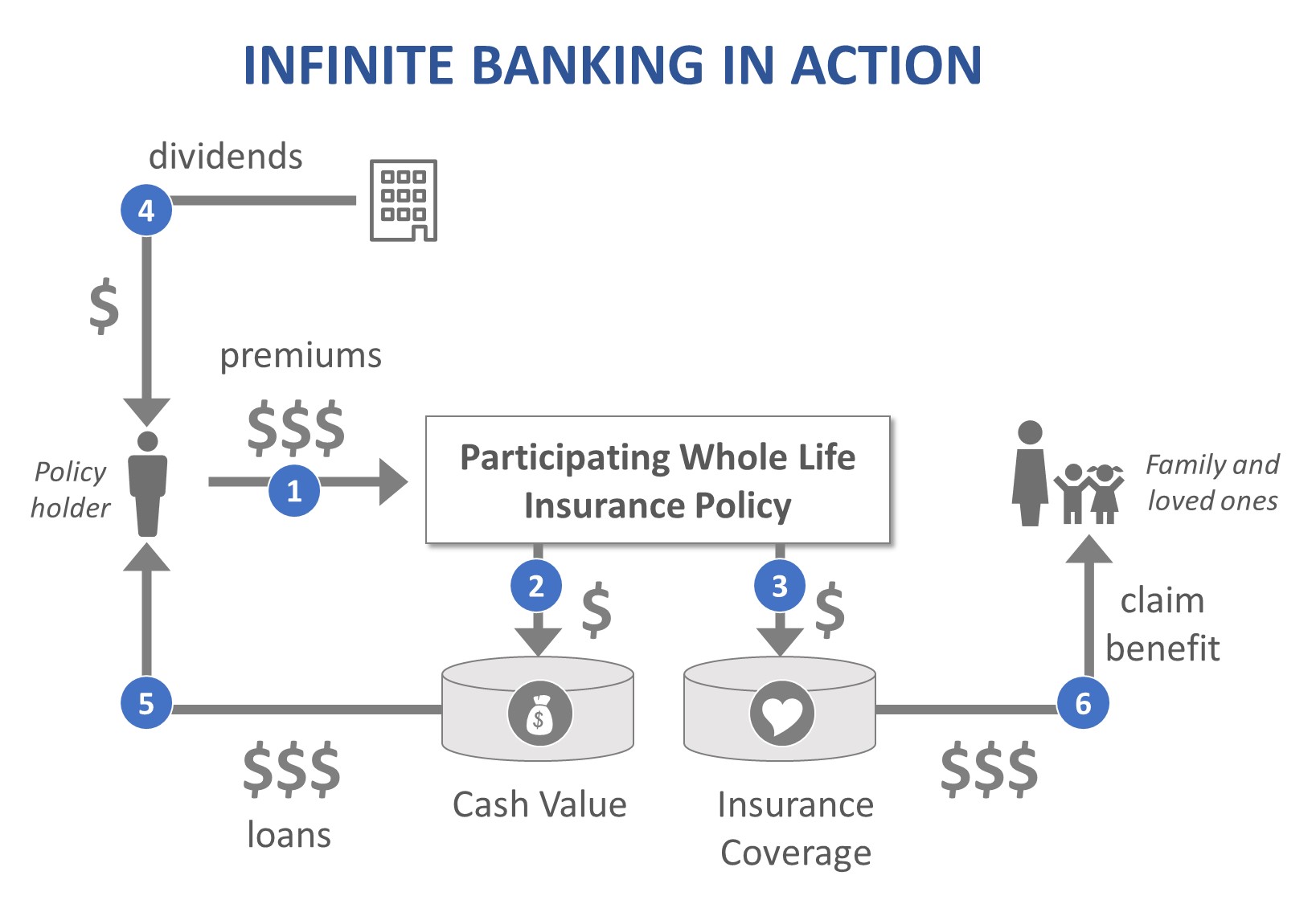

A PUAR permits you to "overfund" your insurance plan right up to line of it coming to be a Changed Endowment Contract (MEC). When you make use of a PUAR, you rapidly raise your cash worth (and your death advantage), thereby increasing the power of your "financial institution". Additionally, the more cash money worth you have, the greater your interest and returns repayments from your insurer will be.

With the increase of TikTok as an information-sharing platform, financial guidance and methods have actually located an unique method of dispersing. One such strategy that has actually been making the rounds is the unlimited banking idea, or IBC for short, garnering recommendations from celebrities like rapper Waka Flocka Flame. Nevertheless, while the method is currently preferred, its roots map back to the 1980s when economist Nelson Nash presented it to the globe.

What are the common mistakes people make with Private Banking Strategies?

Within these plans, the cash value expands based upon a rate set by the insurer (Bank on yourself). Once a significant cash money worth collects, insurance holders can get a cash money worth car loan. These loans vary from conventional ones, with life insurance policy acting as collateral, meaning one could lose their insurance coverage if borrowing excessively without appropriate cash value to sustain the insurance expenses

And while the allure of these plans appears, there are inherent restrictions and threats, necessitating thorough money value tracking. The technique's authenticity isn't black and white. For high-net-worth individuals or business owners, particularly those making use of approaches like company-owned life insurance policy (COLI), the benefits of tax breaks and compound development can be appealing.

The appeal of infinite banking does not negate its challenges: Price: The foundational requirement, a long-term life insurance policy policy, is more expensive than its term counterparts. Eligibility: Not every person gets entire life insurance coverage because of extensive underwriting processes that can omit those with particular health and wellness or way of living problems. Complexity and threat: The complex nature of IBC, paired with its threats, might deter several, specifically when simpler and less dangerous choices are available.

Who can help me set up Cash Value Leveraging?

Alloting around 10% of your regular monthly revenue to the plan is just not viable for the majority of people. Making use of life insurance policy as a financial investment and liquidity source requires discipline and monitoring of policy cash value. Consult a financial expert to determine if boundless financial aligns with your concerns. Part of what you review below is simply a reiteration of what has already been claimed above.

So before you get yourself into a circumstance you're not planned for, understand the following first: Although the idea is generally sold as such, you're not really taking a financing from yourself. If that were the instance, you would not have to settle it. Rather, you're borrowing from the insurer and need to repay it with passion.

Some social media articles advise making use of cash money worth from whole life insurance policy to pay for charge card financial debt. The idea is that when you settle the funding with rate of interest, the amount will certainly be returned to your investments. Unfortunately, that's not exactly how it functions. When you repay the loan, a section of that passion mosts likely to the insurance provider.

For the very first several years, you'll be settling the payment. This makes it very tough for your plan to gather worth during this time around. Whole life insurance policy prices 5 to 15 times a lot more than term insurance policy. Lots of people simply can not afford it. So, unless you can afford to pay a couple of to numerous hundred dollars for the following decade or more, IBC won't help you.

Is there a way to automate Privatized Banking System transactions?

If you require life insurance, below are some beneficial suggestions to think about: Take into consideration term life insurance coverage. Make sure to go shopping about for the ideal rate.

Picture never ever having to fret regarding bank finances or high passion rates once again. That's the power of infinite banking life insurance.

There's no set finance term, and you have the liberty to pick the settlement timetable, which can be as leisurely as paying off the financing at the time of death. Financial independence through Infinite Banking. This versatility reaches the maintenance of the lendings, where you can go with interest-only payments, keeping the financing balance flat and manageable

Holding cash in an IUL repaired account being attributed rate of interest can typically be far better than holding the cash money on down payment at a bank.: You've always desired for opening your own pastry shop. You can borrow from your IUL policy to cover the first costs of leasing a room, buying tools, and hiring staff.

Can I use Infinite Banking Concept to fund large purchases?

Individual fundings can be gotten from traditional financial institutions and lending institution. Below are some bottom lines to consider. Bank card can offer a versatile way to borrow cash for extremely temporary durations. However, borrowing money on a charge card is usually really expensive with annual percentage rates of rate of interest (APR) commonly getting to 20% to 30% or even more a year - Infinite Banking retirement strategy.

{kind=link}

Latest Posts

Privatized Banking Concept

Infinite Banking Definition

Infinite Banking Concept Example